turn on the TV or radio these days and you're almost guaranteed to hear an advertisement for car insurance but when it comes to buying or choosing the right insurance what do you really need your first step in finding the right policy is to make sure you meet the state's minimum insurance

requirements if you don't know your state's requirements visit the insurance commissioners website for your state or call their office they're happy to help you get started but what about all the types of coverage and services that are offered what do you need to really be protected on the road an easy way to think about auto coverage is in terms of to whom the benefits will be paid personal coverage pays you as the vehicles owner liability coverage pays others for damages you're legally responsible for as the result of an accident first we'll focus on coverages that benefit you as the policyholder there are two types of physical damage coverage available with car insurance policies collision coverage and comprehensive coverage collision and comprehensive coverage are similar that they both cover the loss related to your vehicle

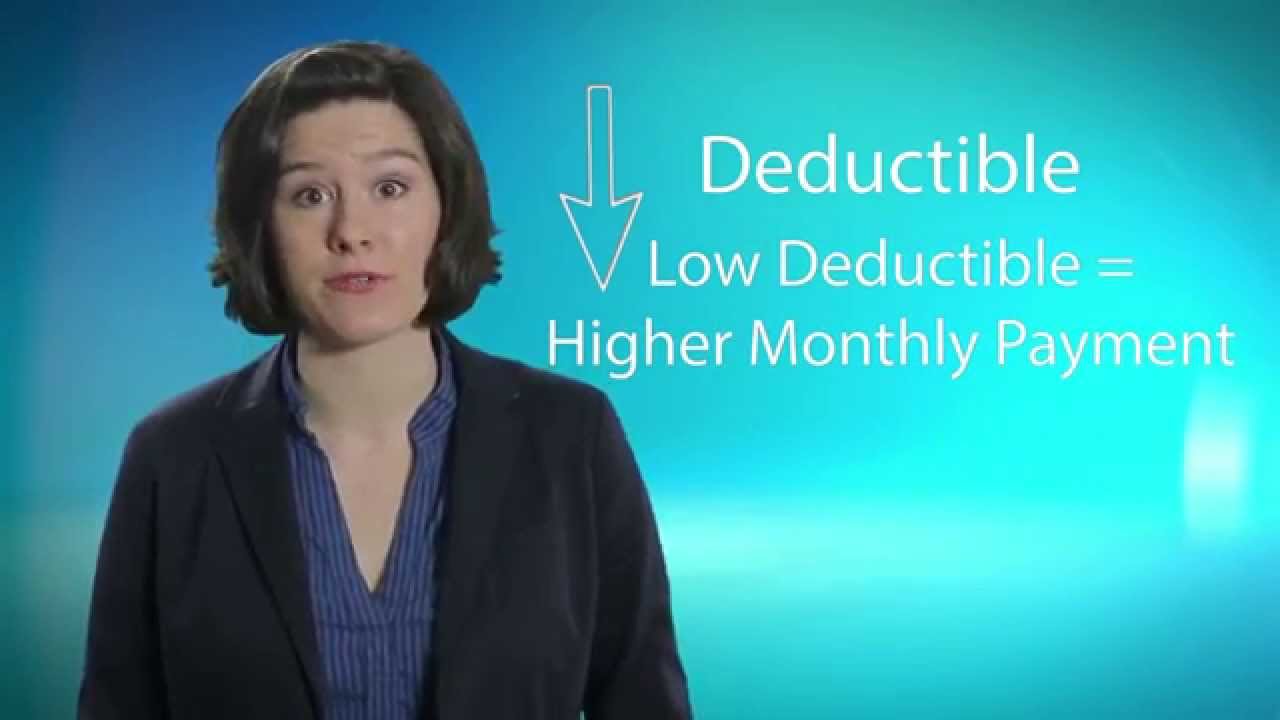

however collision insurance specifically covers damage caused by accidents with other vehicles and stationary objects like trees or road signs even potholes it is important to remember that collision coverage only handles repair and replacement costs up to your vehicle's actual cash value your vehicles actual cash value is not how much you paid for it or still owe the loan instead the actual cash value is the vehicle's current value considering factors like it's age mileage and condition with this coverage you'll be asked to select a deductible the deductible is the amount you'll be responsible for paying for each covered loss but more about deductibles in a moment the second type of damage coverage for your vehicle is comprehensive this covers damages your vehicle incurs from non accident events like weather wind hail or ice as well as theft and vandalism two other types of personal coverage you should consider are rental reimbursement and gap insurance rental reimbursement pays for a rental vehicle if your car is not drivable as the result of a cupboard or insured loss it is optional and not required as part of your insurance policy however it can be beneficial if your car must be in the repair shop for several days and if you do not have access to another vehicle if your vehicle is financed you may also want to consider gap insurance this pays the difference between the actual cash value of a vehicle and the balance still owed to a lien holder or in a car loan or lease program it helps prevent you from being upside down on your loan or owing the bank more than the actual cash value in the result of a total loss situation however before you purchase this coverage from your insurance agent be sure to check your loan or financing agreement many times gap insurance is a part of a loan agreement when you purchase the vehicle however double check to make sure you don't already have gap insurance now let's talk about deductibles basically a deductible is the amount of money you must pay when making a claim on your policy before your insurance company begins paying additional costs for example suppose you have a policy with a $500 deductible and you have an accident that causes $3,000 in damages to your vehicle you are responsible for the first 500 dollars of repairs the insurance company pays the remaining 2,500 dollars of repairs the amount of the deductible you choose makes a difference in the amount of your insurance premium a low deductible means a higher premium a high deductible means a lower premium however it is possible that should you be in an accident your deductible might not fit your budget if your budget allows for a high out-of-pocket expense choosing a high deductible might be worthwhile for the lower premium however if a high deductible is not in your budget a higher premium may be best for you all of us on the road at some point have worried about the dangers of an uninsured or underinsured driver causing an accident that's why uninsured motorist coverage can be a financial lifesaver uninsured or underinsured motorist coverage provides reimbursement if you are involved in an accident with a driver who doesn't have sufficient or any liability insurance without this type of coverage you could be stuck with a hefty repair bill and medical bills you'd if the accident was not your fault the key with this coverage is that it pays damages that are not covered under the physical damage coverage of your policy and its limits with medical payment coverage with an increase in uninsured drivers over the last few years this is a critical coverage to consider adding to any insurance policy property damage insurance covers the cost of repairs for damage done to another person's property in an accident it also covers court costs and legal expenses United States law requires drivers to carry at least $5,000 property damage coverage per accident however the minimum in States is higher remember the minimum amount most likely will not cover all the expenses in a serious accident most car insurance professionals recommend at least $50,000 of property damage liability insurance many consider one hundred thousand dollars per accident the ideal amount in 2013 the average price of a car was $31,000 you can see how quickly damages can add up if multiple vehicles are involved we don't have time to cover all the different types of insurance available however we hope this has helped explain some of the more common types of insurance you can get for your automobile if you have any more questions we're always here to help drive safe

التسميات

car insurance